When two people decide to merge their financial lives, budgeting becomes one of the pillars of their shared success. Money is often cited as a leading cause of relationship stress; a 2023 survey from the American Psychological Association revealed that 31% of couples cite finances as a primary source of conflict. Consequently, mastering budgeting as a couple isn’t just about managing money—it’s about fostering trust, communication, and long-term goals. This article explores practical tools and strategic approaches that couples can use to optimize their collective finances, improve transparency, and sustain healthy financial habits together.

Understanding Joint Financial Management

Joint financial management is more than pooling incomes or splitting expenses; it’s about creating a framework within which two individuals with potentially differing attitudes toward money can align. Establishing a clear budget as a couple helps reduce ambiguity about spending priorities—for example, deciding whether saving for a home takes precedence over monthly outings.

Consider the case of Sarah and James, a couple living in Portland, Oregon. Both had different spending patterns – Sarah was a saver, James a spender. They initially tried managing money separately but often clashed during monthly expense reviews. When they opted to build a joint budget using shared tools, their communication improved, and they successfully saved $15,000 for a down payment over 18 months.

According to a 2022 study by the National Endowment for Financial Education (NEFE), couples who create budgets together report 35% less financial stress and show a 50% higher rate of achieving joint savings goals than those who don’t. This demonstrates not just the importance but the efficacy of budgeting together.

Common Budgeting Approaches for Couples

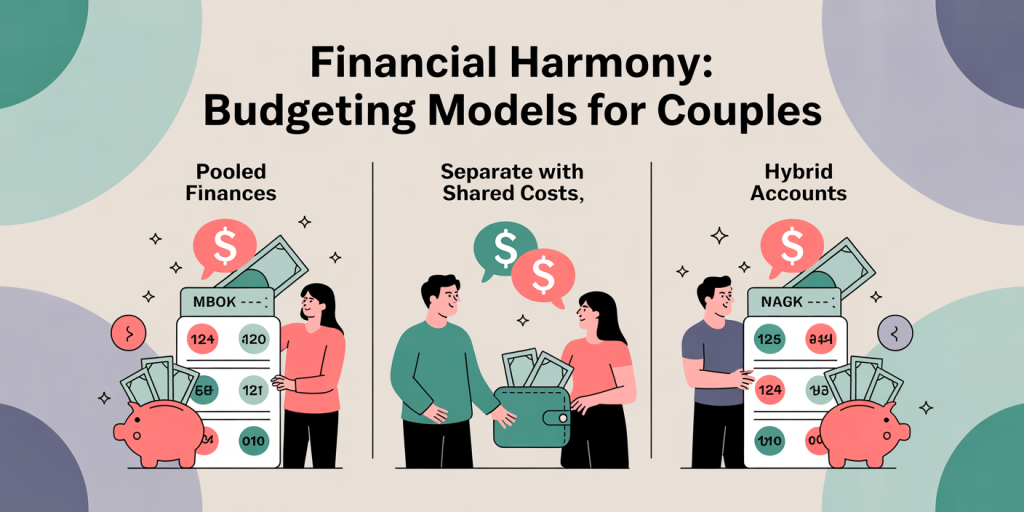

Couples tend to follow one of three budgeting models: pooling all income and expenses, maintaining separate finances while splitting shared costs, or a hybrid approach combining elements of both methods. Each approach suits different relationship dynamics and financial situations.

Pooling Finances: This method involves combining incomes into a single account from which all expenses and savings derive. For instance, Anna and Leo combined their salaries into one checking account. They tracked common expenses such as rent, groceries, and utilities transparently. This model encourages complete financial integration but requires high levels of trust and communication.

Separate Finances with Shared Costs: Alternatively, couples like Mia and Jordan maintain separate accounts but agree on sharing fixed costs proportionally based on income. If Mia earns $4,000 monthly and Jordan $6,000, they might split the $2,000 rent as $800 from Mia and $1,200 from Jordan. This preserves financial independence but requires careful record-keeping and clear rules around shared spending.

Hybrid Approach: Sometimes couples mix these styles. For example, a joint account covers recurring bills and savings, while discretionary spending remains individualized. This offers both shared responsibility and personal freedom.

| Budget Model | Advantages | Potential Challenges | Best For |

|---|---|---|---|

| Pooled Finances | Full transparency, streamlined management | Requires trust and communication | Long-term committed couples |

| Separate Finances with Shared Costs | Maintains independence, flexible | Complex logistics, possible disputes | Couples valuing autonomy |

| Hybrid Approach | Balanced control and sharing | Can be confusing without clarity | Couples seeking compromise |

Understanding these models lets couples select the framework that aligns with their values and lifestyle.

Digital Tools Enhancing Couples’ Budgeting

Technology revolutionizes budgeting for couples by offering shared visibility, automation, and real-time updates. The rise of financial apps specifically designed for joint use ensures couples remain coordinated without cumbersome spreadsheets.

YNAB (You Need A Budget): YNAB emphasizes proactive budgeting, encouraging users to assign every dollar a purpose. Couples can connect their accounts jointly, allowing both partners to monitor spending in categories like groceries or entertainment. Its collaborative features ease joint decision-making.

Honeydue: Tailored for couples, Honeydue tracks bills, shared expenses, and individual transactions while offering chat functionalities. For example, Olivia and Ben used Honeydue to settle periodic bills effortlessly and communicate about discretionary purchases, reducing misunderstandings.

Splitwise: While primarily an expense-sharing app, Splitwise helps couples who maintain some separate finances but want to keep track of shared expenses such as vacations or dinners. It logs who paid what and calculates owed amounts automatically, simplifying reimbursements.

Studies from a 2021 report by FinanceBuzz highlight that 68% of couples using budgeting apps experience reduced conflict regarding finances. These tools not only aid transparency but also support mutual accountability.

Strategies for Effective Communication and Goal Setting

Budgeting success hinges on effective dialogue and shared goals. Couples who avoid discussing money often fall into traps of suspicion and unmet expectations. Establishing regular financial check-ins fosters a safe space for adjustments and celebrations of milestones.

Start by discussing priorities. For example, a couple might prioritize emergency savings, then retirement contributions, followed by discretionary spending. This order helps prevent impulsive expenditures and aligns decisions with long-term security.

Setting SMART goals—Specific, Measurable, Achievable, Relevant, Time-bound—is essential. Sarah and James, mentioned earlier, applied this by targeting a $15,000 home down payment in 18 months. They broke it down monthly ($833.33) and reviewed progress quarterly using their shared budgeting app.

Conflict resolution is an inherent part of joint budgeting. Techniques such as “active listening” and “I” statements (e.g., “I feel concerned when…” rather than “You always overspend”) de-escalate tensions and encourage collaboration. Financial counseling can help couples navigate persistent challenges and improve money communication.

Managing Debt and Savings as a Unit

Couples often navigate complex scenarios involving individual debts such as student loans or credit cards, alongside joint savings aspirations. Approaching these together is critical to avoid hidden triggers and foster financial unity.

A practical strategy involves full disclosure of liabilities early in the relationship and integrating debt repayment into the couple’s budget. For example, Emily and Raj faced $30,000 in combined student loans. They created a debt snowball plan prioritizing the smallest balance first and committed an extra $500 monthly toward repayments from their pooled account.

On the savings side, couples benefit from both joint and individual funds. A joint emergency account covering 3-6 months of living expenses safeguards financial stability. Simultaneously, individual “fun money” allowances prevent resentment and maintain autonomy.

A comparative glance at joint versus separate debt repayment approaches illustrates differing outcomes:

| Debt Repayment Approach | Benefits | Drawbacks | Suitable For |

|---|---|---|---|

| Joint Repayment | Streamlined payments, collective motivation | Risk of unequal burden if incomes differ | Couples with shared financial goals |

| Separate Repayment | Maintains autonomy, less conflict | Slower progress, potential for misalignment | Higher-earning partner prioritizes |

By tailoring debt and savings management to their unique dynamics, couples enhance financial resilience.

Future Perspectives: Adapting Budgeting for Changing Circumstances

Financial lives evolve due to income fluctuations, family growth, career changes, or economic shifts. Couples need budgeting approaches and tools that provide flexibility and adaptability sustained over time.

For instance, when a couple welcomes a child, expenses increase significantly. According to the U.S. Department of Agriculture (2023), the average cost of raising a child to age 18 is approximately $284,570. Couples like Megan and Tyler adjusted their budget by increasing their joint savings rate, cutting discretionary spending, and revisiting their financial goals to include education funds.

Additionally, inflation impacts require periodic reassessments of budgets. The Consumer Price Index rose 5% in 2023 compared to the previous year, urging couples to update their budgets to ensure that savings targets remain realistic.

Looking forward, advancements in AI-powered financial management tools promise to revolutionize couple budgeting. These platforms will offer predictive analytics based on spending patterns and personalized recommendations, allowing partners to plan proactively.

Moreover, financial education tailored for couples is gaining recognition as a necessary resource. Programs addressing communication, goal alignment, and budgeting techniques can empower couples before conflicts arise.

Overall, the best budget strategies for couples are those that evolve alongside their journey, remain transparent, and foster mutual respect.

Budgeting as a couple requires intentional choices, open communication, and effective tools. Whether they pool incomes fully, divide responsibilities, or find a hybrid solution, couples benefit from clear frameworks and digital aids. By prioritizing shared goals, addressing debt together, and adapting plans to life changes, couples can transform budgeting from a contentious chore into a collaborative endeavor that strengthens their partnership and financial security.

Deixe um comentário